UK Credit Cards: Are "Established" Accounts in Trouble?

FICO data reveals worrying trends developing amongst established credit card users as missed payments rise

We have recently analysed UK personal credit card trends and found worrying payment patterns amongst customers who have held their cards for between one and five years, known as the Established vintage. This group is showing increased rates of missed payments and other signs of financial stress. This will particularly be a concern for risk managers, with new Consumer Duty expectations starting in July.

Here are some of the key trends we observed:

- Established vintage of UK credit card accounts is 83 percent more likely to have missed two payments in February 2023 than the average of all credit card accounts

- The average balance value predicted to not be paid by the Established group is 69 percent higher than for all credit card accounts for February 2023

- The percentage of accounts with three missed payments is nearly 94 percent higher amongst Established card holders than for all credit card accounts for February 2023

We analysed the performance of different groups of cardholders as the pressures of the cost of living crisis increase. In particular, FICO has looked at the Established group – accounts that have been open from one to five years.

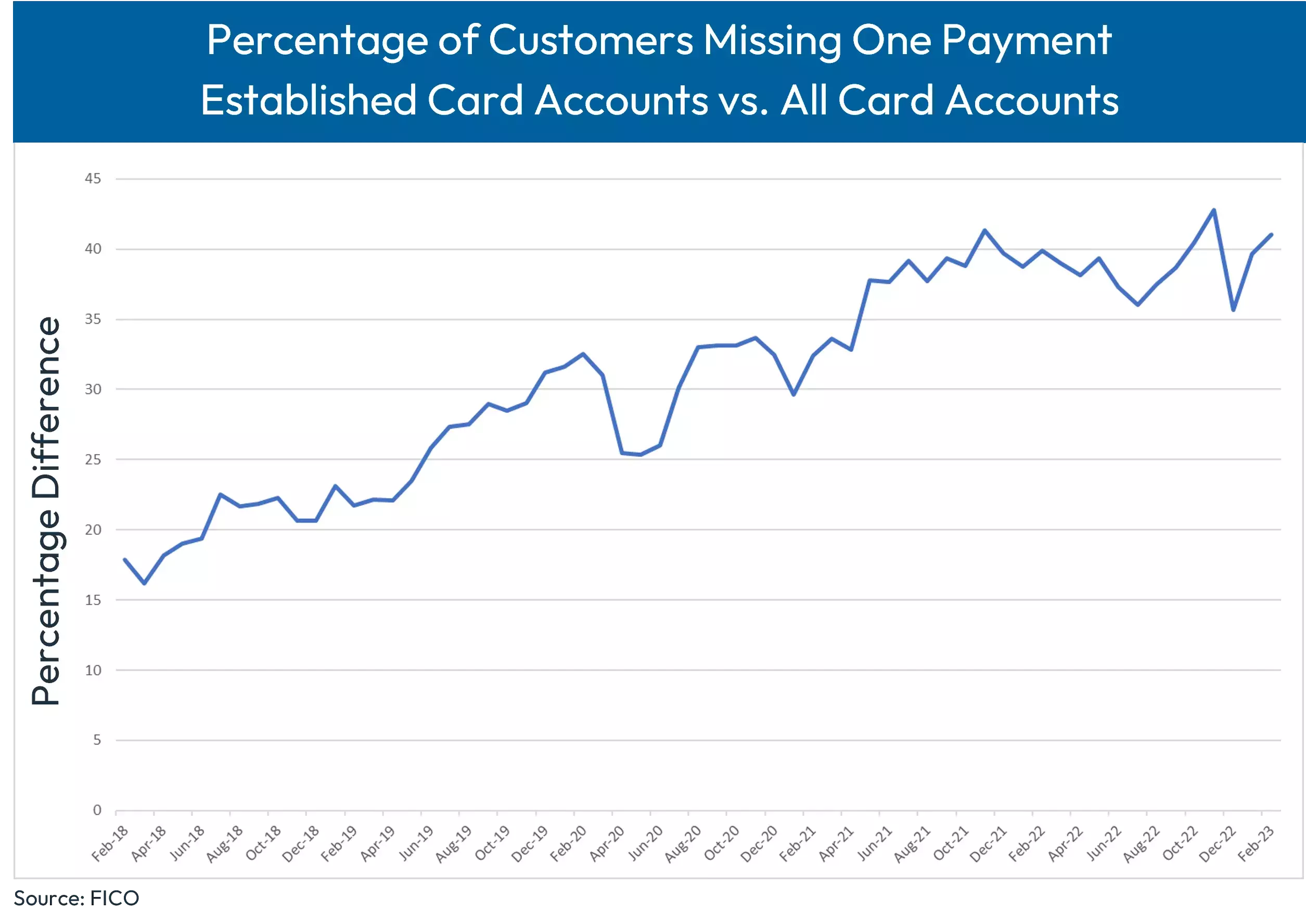

Tracking the difference month on month over a five-year period, the percentage of customers missing one, two and three payments on their credit cards as well as the balance of these missed payments compared to the overall balance are all increasing significantly, as seen by the percentages below:

- The percentage of Established UK credit card accounts with one missed payment is 41 percent higher than all account vintages. It was 18 percent higher in 2018.

- The percentage of Established UK credit card accounts with two missed payments is more than 83 percent higher than all account vintages. It was 53 percent higher five years ago.

- The percentage of Established UK credit card accounts with three missed payments is nearly 94 percent higher. It was 66 percent higher in February 2018.

Vintage Analysis

In line with the higher rate for late payments, the percentage of payments that are less than the minimum due are also considerably higher for the Established group; in February 2023 the average minimum due for Established accounts was 55 percent higher than all accounts.

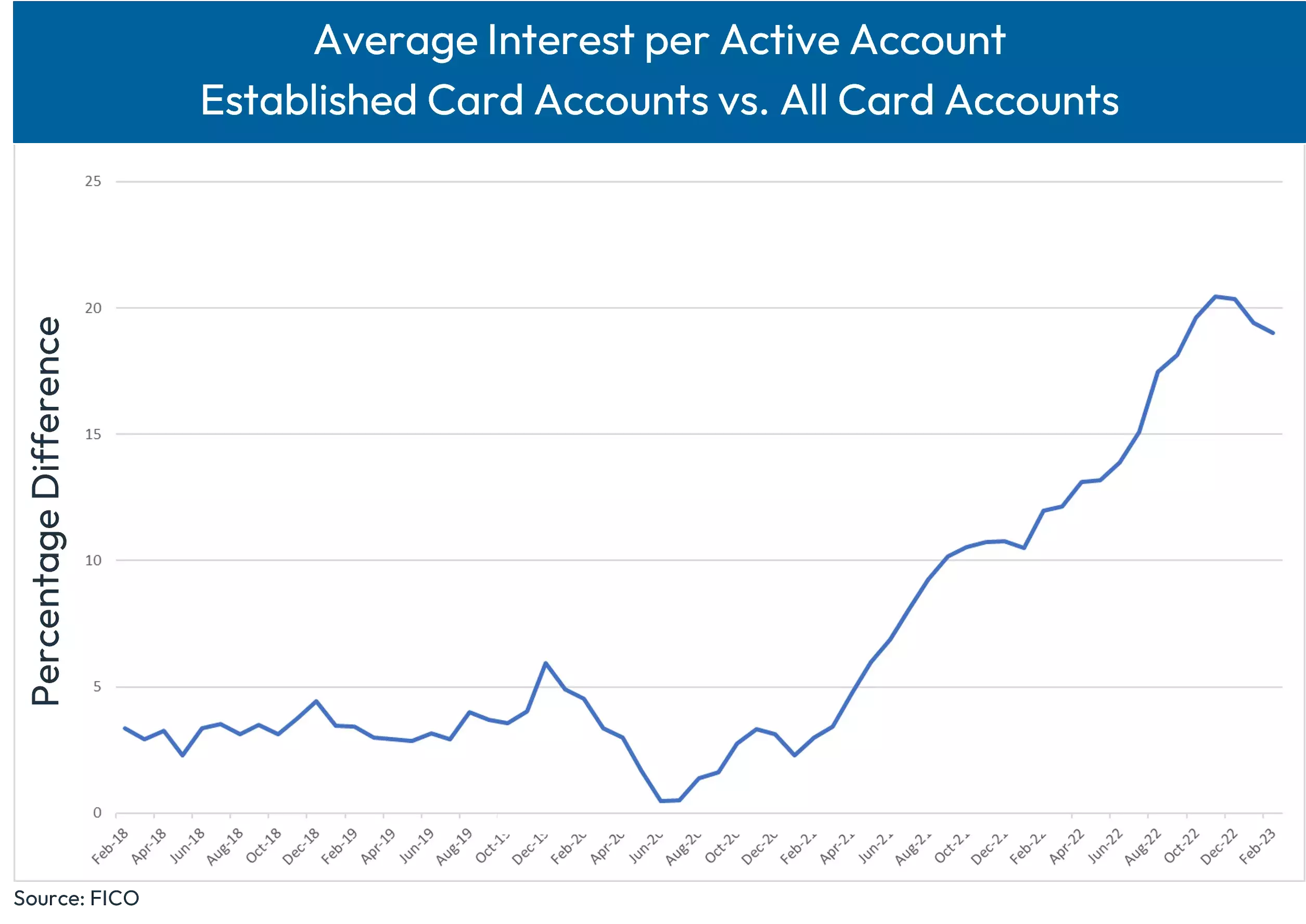

Another key factor is that as customers miss payments, those on a promotional rate will probably have to pay interest, even if they were on a 0 percent balance transfer. As FICO has seen with the increased delinquency for the Established group, average interest per active account is also higher and currently stands 19 percent higher, having risen steeply since July 2020.

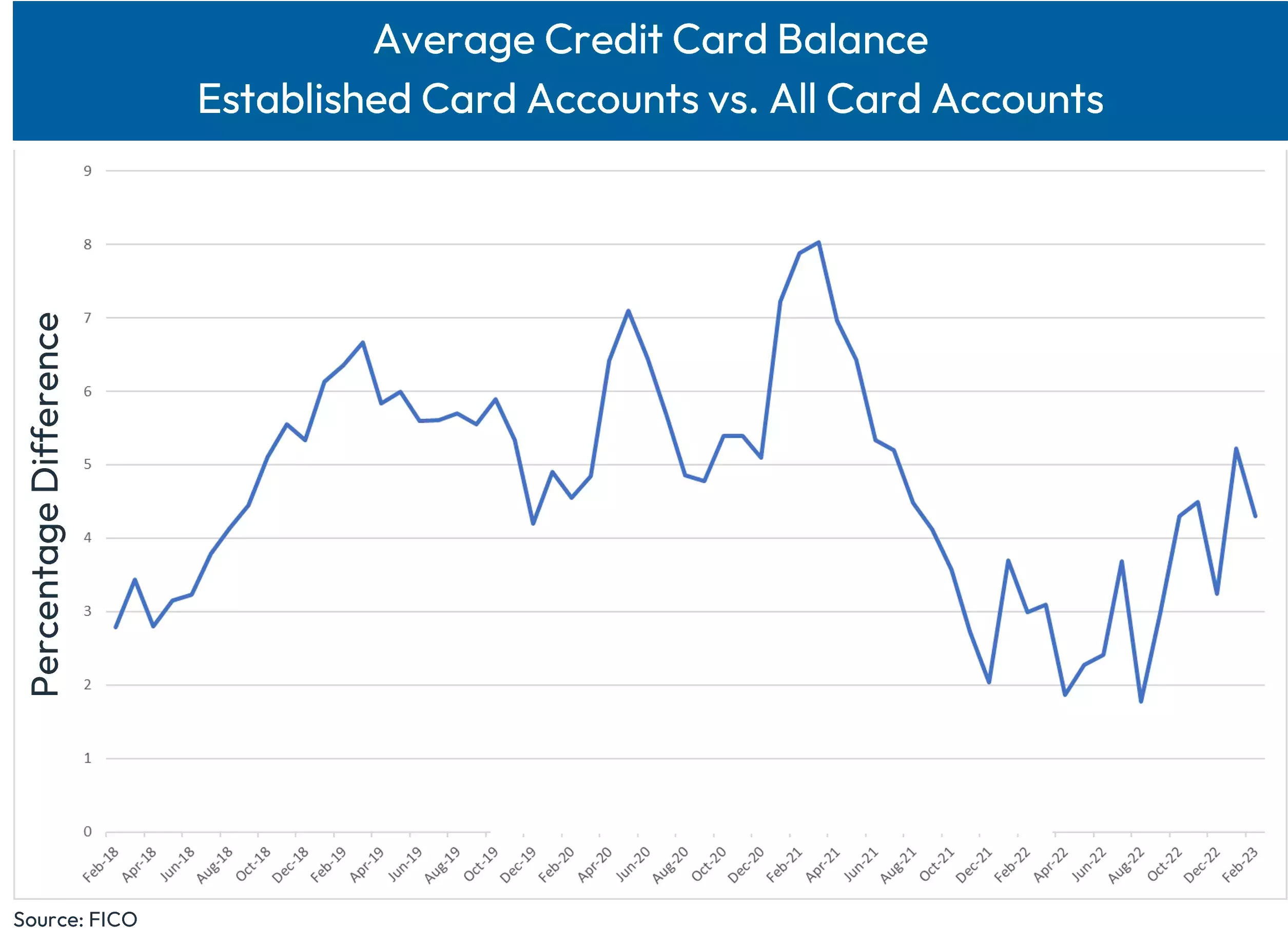

Balance at Risk

FICO’s benchmarking also tracks the “balance at risk” for a customer. This predicts how much of the credit card balance is expected to not get paid. When comparing the Established pool to the overall population during the pandemic, reduced spend opportunities and higher savings lowered the balance at risk. However, since February 2022, this has been increasing in line with the cost-of-living crisis and the average is currently more than 60 percent higher for the Established group. In comparison, the average Established cards balances at risk was 47 percent higher than all vintages in 2018.

All of these trends will be of concern to risk managers. Customers who have taken advantage of promotional offers in the past may now be struggling to transfer these balances elsewhere and are left with higher balances, on a high interest rate with a higher minimum due each month. One of the main themes of the FCA Consumer Duty which comes into force in July is around identifying and supporting vulnerable customers just like these. Proactive treatment and support — such as specific collections treatment, loan consolidation or alternative product offerings with a lower APR attached — are all areas issuers can consider in order to meet the requirements set out in the Consumer Duty.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80 percent of UK card issuers.

How FICO Can Help You Manage Credit Card Risk and Performance

- Work with our FICO Advisors team

- Explore our solutions for credit line management and collections prevention

- See my post on UK Credit Card Trends: From 2008 Crash to Cost-of-Living Crisis

- Read more posts on UK cards

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.