Fraud in the Age of AI: What Global Financial Institutions Are Telling Us

The fraud landscape isn't just evolving — it's transforming. And the data proves it.

Finextra Research, in association with FICO, surveyed 202 fraud management professionals across NORAM, EMEA, LATAM, and APAC to understand how fraud is changing, how organizations are responding, and where the critical gaps in enterprise fraud strategy remain. The findings are a global wake-up call.

Fraud is no longer a contained operational risk. It has become a sustained, enterprise-level financial threat — one that is being turbocharged by artificial intelligence. From deepfake-enabled account takeovers, sophisticated AI-based bot attacks, to AI-generated social engineering at scale, the threat curve has gotten dramatically steeper. And the industry's response, while showing real momentum, has an opportunity to accelerate the impact and scope of their prevention efforts.

Key Takeaways

AI is supercharging fraud at a large scale.

Fraud attempts have surged dramatically, with 26% of organizations reporting increases of over 51% in the past two years. AI has lowered the barrier to entry for fraudsters, driving synthetic identity creation, deepfake-enabled account takeovers, systemic and automated AI-driven bot attacks, and large-scale social engineering attacks aimed at scamming potential victims, that were once only possible for sophisticated criminal networks.

Most organizations recognize the problem but haven't solved it yet.

While 99% of organizations acknowledge the need for a unified, enterprise-wide fraud strategy, only 28% have fully deployed AI/ML-driven fraud detection at scale. The biggest obstacle isn't technology, it's integration. 47% of the respondents citing difficulty embedding AI effectively into their existing fraud control frameworks.

False positives are a significant hidden cost.

One in three organizations reports high or very high false positive rates, which erode customer trust and drive churn, particularly in high-growth digital markets like APAC (50% high/very high). EMEA's relatively strong performance suggests that regulatory maturity and optimized systems can meaningfully reduce this problem.

Orchestration is the missing link.

Fragmented, siloed fraud tools leave gaps even when individual models are sophisticated. The organizations best positioned to win are those building unified decisioning frameworks that orchestrate internal models, third-party vendor intelligence, and consortium data in real time across channels, products, and customer journeys.

The next frontier is agentic AI — and investment is spreading across multiple priorities.

Nearly all organizations (99%) plan to leverage agentic AI within 24 months. Investment is broadly distributed across identity verification, AI/ML detection, and real-time decisioning, signaling that institutions understand there's no single silver bullet: resilience requires advancing on multiple fronts simultaneously.

The Rising Cost of Fraud: Volume, Losses, and AI as an Accelerant

Over a quarter of organizations (26%) have seen fraud attempt increases of more than 51% over the past 24 months, and 22% report fraud-related financial losses increasing by the same margin. Higher attempt volumes are translating directly into monetary impact, a signal that organizations are not yet absorbing or deflecting these attacks effectively enough.

What's driving this surge? Artificial intelligence in the hands of fraudsters. AI has become a great equalizer, enabling previously unsophisticated bad actors to execute attacks that were once the exclusive domain of advanced criminal organizations.

Application fraud — including synthetic identity creation and account takeover — is among the fastest-growing threats. Synthetic identity fraud is seeing its greatest increase in the 61–80% growth range, with NORAM and APAC leading high-end growth at 14% reporting increases above 81%. This type of application fraud is particularly insidious: fraudsters build seemingly legitimate customer profiles over time, bypassing traditional fraud prevention controls until losses finally materialize.

Critically, every major fraud vector scored 4.3 or above out of 5 when organizations rated the impact of AI-enabled fraud, and all scores fell within a narrow 0.22-point range globally. This tight clustering signals something important: organizations are no longer facing one dominant fraud type. They are facing simultaneous, distributed attacks across every vector at once.

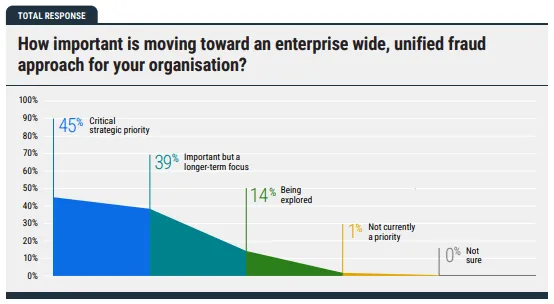

The Enterprise Fraud Challenge: A Gap Between Ambition and Execution

Nearly every organization surveyed (99%) recognizes the need for an enterprise-wide, unified approach to fraud prevention. Yet recognition and execution are not the same thing.

Only 28% of organizations have fully deployed AI/ML-driven fraud detection models operating at scale. At most, 34% have fully deployed any of the three core AI use cases surveyed: Gen AI for customer engagement support, Gen AI case management assistance, and AI/ML-driven detection models. The majority of financial institutions are still somewhere between piloting and limited production deployment.

This deployment gap is not primarily a technology problem. Nearly half of organizations (47%) cite difficulty integrating AI effectively as their primary challenge, ahead of increasing fraud complexity (40%), regulatory constraints (35%), data governance issues (34%), and legacy system limitations (32%).

Fraud modeling capabilities have frequently outpaced orchestration maturity. The result is that many organizations have advanced AI tools that are not yet meaningfully connected across channels, products, and portfolios. Without connected data, even the most sophisticated AI models cannot perform to their potential, allowing enterprise fraud to slip through the gaps.

False Positives: The Hidden Cost of Incomplete Fraud Prevention

The pressure to detect more fraud is creating a secondary problem: one in three organizations (33%) reports "high" or "very high" false positive rates from their fraud detection systems.

This matters because false positives are not just an operational inconvenience. When legitimate transactions are flagged as suspicious, customers face delays, extra verification steps, or declined services. That friction erodes trust, damages customer experience, and increases churn, particularly in rapidly expanding digital markets.

APAC records the highest overall "high/very high" false positive rate at 50%, with 20% reporting "very high", reflecting the pressures of rapid digital payments adoption outpacing control optimization. NORAM also reports high false positive rates (41% "high/very high") despite mature infrastructure — a sign that even well-funded environments struggle when fraud attempts become more sophisticated and targeted.

EMEA offers a contrasting benchmark: 44% of EMEA respondents report low false positives, ranking 20 percentage points above other regions, suggesting that regulatory alignment and more mature systems can help organizations strike a better balance between protection and customer experience.

The takeaway for fraud prevention leaders is clear: reducing false positives is not separate from stopping fraud. It is part of the same challenge. Adaptive, risk-based orchestration informed by better data signals, consortium intelligence, and continuous feedback loops is what allows organizations to tighten controls without creating friction that erodes the trust they've worked hard to build.

Orchestration Is the Keystone

If there is a single theme that runs through this research, it is this: the organizations that will win are those that move beyond fragmented, siloed fraud management to unified, AI-enabled orchestration.

Third-party vendor models are currently the most integrated and most influential in fraud decision-making — 41% of financial institutions say they have the greatest influence on their fraud decisions, compared to 28% for in-house models. This reflects the value of partnering with specialist vendors who can continuously tune models against evolving fraud typologies at scale and speed that in-house teams often cannot match.

But true resilience requires integrated decisioning frameworks that connect internal models, external vendor intelligence, and consortium data — in real time, across the full customer journey.

Virtually all organizations surveyed (99%) plan to leverage agentic AI in their fraud prevention strategy within the next 24 months — though expectations about the role it will play vary considerably, from core autonomous decision-making to an assisted, human-supervised function. EMEA shows the strongest confidence here, with 62% of organizations expecting agentic AI to play a core or autonomous role.

Where Investment Is Headed

Given all of the above, where are financial institutions prioritizing their fraud-related investment over the next 24 months?

Identity verification and authentication and AI/machine learning for fraud detection tie as the top investment areas, each cited by 16% of organizations as their largest share of investment. Real-time decision-making ranks second at 12%, followed by operational efficiency at 11%. The fact that investment priorities are closely clustered within just a 1.03-point range tells its own story: organizations recognize that there is no single silver bullet. Strengthening enterprise fraud resilience requires balancing multiple initiatives simultaneously.

Notably, minimizing customer friction ranks last among investment priorities, suggesting that as fraud grows in volume and complexity, organizations are prepared to accept some trade-off in customer experience in the near term to get protection right. The goal, however, must be to eventually eliminate that trade-off entirely through smarter orchestration.

The Path Forward: Four Priorities

The data in this research points to four immediate priorities for financial institutions:

First, close the deployment gap by moving AI from pilot to production at enterprise scale, prioritizing what works within disciplined fraud control frameworks rather than launching yet more pilots.

Second, invest in active orchestration across models, channels, products, and portfolios so that shared signals shape fraud management decisions in real time.

Third, apply risk-based, outcome-driven prioritization to balance competing investment demands, led by financial impact and regulatory exposure.

And fourth, treat fraud prevention and customer experience as a single, connected challenge. The organizations that can do both will be the ones that define competitive advantage in this era.

As Gregory Hodges, Head of Trust and Safety at JPMorgan Chase, explains: "AI has enabled bad actors to create attacks faster, at more scale, and with greater precision and quality. Attacks are becoming less manual and are more industrial, with bad actors also using AI to generate synthetic identities by combining real and fake data to create profiles that look, feel, and behave like real customers before eventually unleashing a broad-based fraud attack."

The threat is real, it is accelerating, and it is operating across every fraud vector simultaneously. But so is the opportunity for the organizations willing to move from fragmented pilots to true enterprise fraud transformation.

Want the full picture? Download the complete global survey report, "Fraud in the Age of AI: Trends, Threats, and Management Tactics," for in-depth data, regional breakdowns, and expert commentary from JPMorgan Chase, BNY, and LHV Bank. And watch for our regional eBooks — diving deeper into the specific fraud dynamics, AI deployment maturity, and investment priorities shaping fraud prevention in NORAM, EMEA, LATAM, and APAC.

Frequently Asked Questions

AI has become the primary accelerant, enabling fraudsters to create synthetic identities, execute deepfake-enabled account takeovers, and launch large-scale social engineering attacks with greater speed and precision than ever before.

The main barrier isn't technology, it's integration. Nearly half of organizations (47%) struggle to embed AI effectively within their existing fraud control frameworks, and many are still stuck between pilot programs and full production deployment.

False positives occur when legitimate transactions are incorrectly flagged as fraudulent. Beyond being an operational headache, they create customer friction, damage trust, and increase churn, meaning poor fraud detection hurts the business even when no actual fraud occurs.

Agentic AI refers to AI systems capable of taking autonomous or semi-autonomous actions. In fraud prevention, it represents the next evolution of orchestration — with 99% of organizations planning to incorporate it within the next two years to help connect data, models, and decisions across the full customer journey in real-time.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.