Top 5 Debt Collection Posts for 2020: Pandemic Perspectives

FICO collections experts explored how to deal with the debt tsunami in a series of posts

Posts dealing with debt collection were among the most popular on the FICO Blog last year, for obvious reasons. Fortunately, our bloggers stepped up with timely analyses of the challenges facing lenders in an era of payment holidays, furloughs and higher unemployment. They also offered perceptive tips for dealing with what they dubbed the “debt tsunami.”

Here were the five most popular posts in this category last year:

#1. Debt Collection And Covid-19: What Past Crises Can Teach Us

Bruce Curry brought his experience to bear in a series of posts, beginning with this one. “There were a number of things that we did not do during the last global crisis, the global financial crisis of 2008,” he noted. “In particular, we failed to:

- Identify the customers who would not have been in collections were we not in the situation we are in. Today, that would mean we did not identify the customers entering collections purely because of COVID-19.

- Understand how these particular customers would perform compared to steady-state collections customers:

- We did not profile their behaviours and how they differed in a collection situation.

- We didn't look back at how they had behaved just before they came into the collections area.

- We did not assess how they might behave once the crisis that triggered their financial stress was starting to pass.

- We didn't profile their likely return to financial good and we didn't understand any differences in their financial morality.”

Bruce offered some high-level advice for debt collectors, including an important message around information capture. “Capture important information today that you would not have chosen to capture in the past. When the initial tidal wave of customer calls starts to lessen. there will be large books that need to be worked. Collections, risk and operations executives will need to have the data that helps them:

- Understand the differences between COVID-19 related debt and non-COVID related debt

- Identify the customers that classic collections risk analytics apply to, and those for whom it is it redundant

- Determine the likely return to financial good profile by customer cohort data, including:

- Were they in a protected industry?

- What circumstances drove their reduction of income? E.g. was it:

- Furlough and if so with what degree of protection?

- Redundancy?

- Sickness?

- What has been the true level of impact on disposable income – can open banking support and validate the impact?

- What is their likely return to good curve given their household dynamics and industry sector?”

#2. 8 Success Tips For Debt Collection In The Pandemic

“Collections departments are now bracing themselves for a tsunami of people unable to meet their financial commitments,” Bruce Curry noted in a follow-up post. He shared his eight tips — here’s the first one, where he expanded on the need for more data:

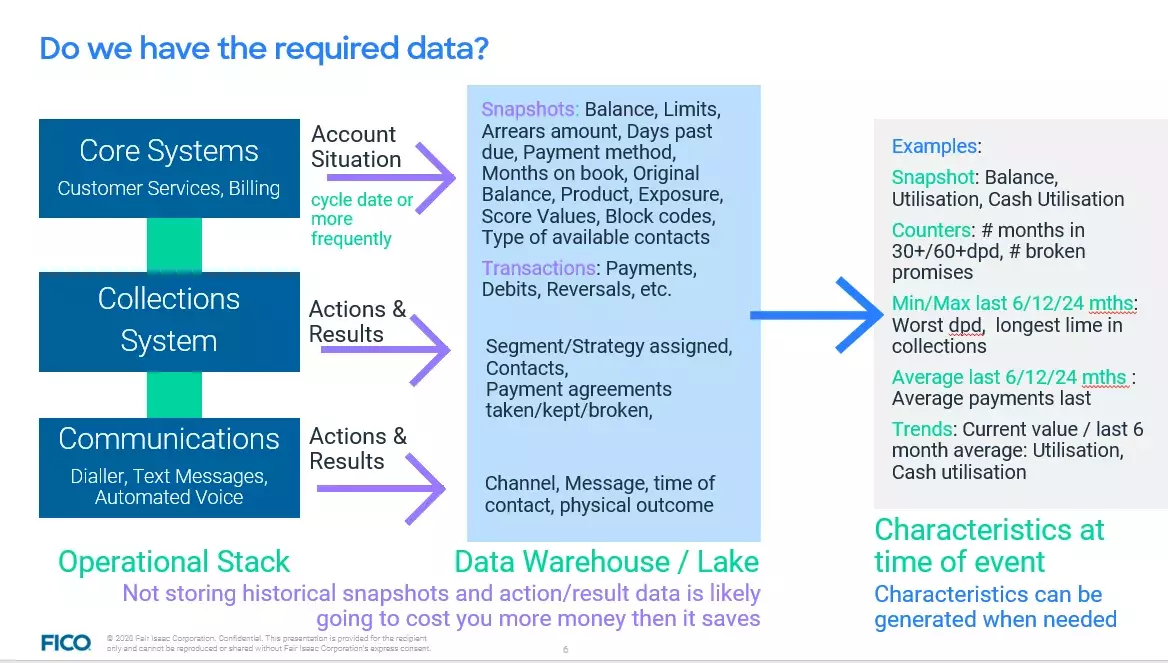

Tip 1 - What data do we need to identify the vulnerable?

It is essential to proactively identify the vulnerable. It is worth repeating that collections departments are now tasked with dealing with thousands of customers who are not in arrears due to the usual reasons and without the usual market data to help identify and segment them. These clients have been furloughed with a rapid, surprising and significant reduction in income and these dramatic changes in circumstance have yet to be detected by credit bureaus.

As an industry we have always been proactive about predelinquency. But now we need to dig deep across our organisations to capture data and find the vital information needed to clearly separate the economic victims from the steady state collections customers.

The data is there – be it from call, collections or communications systems and we need access to this information as it will inform how we talk to our customers who need to be segregated carefully.

- Information that tells us how reliant on credit the customer is, card utilization, renewal of UPLs

- Information that tells us about their financial morality – transactor not revolver, direct debit payer, early settlements of UPLs, takes advantage of interest-free offers, low LTV, lower than average balloon payment in terms, number of credit lines

- For issuers – the changes in card transaction spend type and velocity

- Credit stress – number of new applications for credit internally and at bureau, frequency and degree of overdraft facility

- Whilst rare, any information about their industry, occupation, earning potential, stability (number of address & telephone number changes)

Without much of the above, these customers will end payment holiday periods as low-risk customers. There is a real urgency to understand the true degree of risk on these customers — on which you know little, as they are not normally a collections customer.

Just as this is unlike any other crisis, COVID customers are different. We need to ensure we have or can capture at the earliest possible opportunity, in a format that enables empirical use:

- The reason for delinquency

- The duration of impact

- The disposable income

- Affordability over time

- Industry sector and role within

In addition to our standard data, this information is necessary to help us understand not only their position now, but where they are likely going to be for the rest of this year and beyond. These are customers we are going to have communicate regularly with to understand the changing nature of their personal circumstances.

Three distinct collections phases

There are three distinct pandemic related collections phases – tactical, mid-term and the more strategic long-term. Each requires a different approach to customer segmentation and communication.

- Tactical Phase - Day 1-90: Capturing the correct data to ensure COVID-19 is registered as reasons for the policyholder being delinquent will be critical in relation to both near-term relief and impairment reporting later in the timeframes outlined.

- Mid-Term Day - 90-180: As payment holidays expire, customers will require a pre-contact to ensure the right options are put in place for their best outcome in the longer term. Interaction will be essential at this point and with better segmentation; the customer journey may change to either standard collections solution discussion or longer term forbearance options. In either case, validated affordability will be important.

- Long-Term Strategic - Day 180+: Multiple touch points with the customer will be required to validate their financial/personal wellbeing and understanding the reasons for COVID-19 payment holiday/forbearance will be critical for regulatory reporting.

Volumes will still be high and customer journeys will get more complex as initial volumes flatline. There could be a bigger share of vulnerable customers needing forbearance. Four UK tier 1 lenders have announced an expected £20.2 billion increase on impaired loans. We expect an increased need for digital-led payment plans and a higher demand for loan modification so the longer-term financial impacts can be worked through. Ultimately, companies will have to manage higher impairments and losses, which will attract C-level attention to the overall collections and recovery performance.

To read the rest of Bruce’s tips, read the post and watch this on-demand webinar.

#3. Covid-19 And Debt Collection: What’s Happening In Europe

Mark Whale looked at emerging trends across Europe early on in the pandemic. One of his focuses was customer forbearance:

“Unsurprisingly, the Italian financial services sector was the first in Europe to react when it came to introducing large-scale moratoria on debt repayments for mortgages, small loans and companies revolving credit lines,” Jashan wrote. “As expected, other countries followed suit, with UK banks offering 3-month payment holidays on mortgages and other firms (such as utilities) offering delayed repayments on a case-by-case basis.

“Alongside the management of outgoing expenses, we’ve also seen countries take steps to help with customer income. Largely, countries are following Germany’s ‘Kurzarbeitergeld compensation scheme’. This approach sees a percentage of people’s salaries guaranteed by the government (up to certain thresholds). This approach was particularly successful for Germany during the 2008-09 crisis, resulting in Germany only seeing a 0.9% increase in unemployment and a faster return to prosperity, compared to a 3% increase in unemployment for other Organisation for Economic Co-operation and Development (OECD) countries.

“Ultimately, the purpose of forbearance is to return customers to being up to date, whilst preventing unfair customer outcomes. There have been significant numbers of forbearance requests from customers, and C&R teams will need to exercise discipline regarding when and how forbearance is provided. For example, with government income guarantees, C&R teams should work with customers to consider what levels of forbearance are necessary now, alongside the potential to cause detriment through indebtedness further down the line.”

#4. Payment Holidays: New Tool For Managing The Surge

As governments rolled our payment holidays, the sheer volume of customers requesting them became a challenge of its own. FICO brought a solution to market to help with this, as Ulrich Wiesner discussed.

“We have created a set of digital scenarios that can help lenders, telecommunications providers and other firms meet this urgent need in an automated way. The scenarios, set up in FICO® Customer Communications Services, enable firms to quickly and easily set up new payment schedules that help customers seeking immediate relief.

“With this solution, you can set up CCS to contact the customers by priority: first customers with a high probability of needing a payment holiday, then those with a risk of default or customers whose loans expire in the near future. The outbound contact takes place fully automatically via SMS or telephone and leads the customer through a dialog menu, in the course of which any deferral is clarified and adopted. In exceptional cases, the customer will be passed on to an employee for complete clarification.”

See an example of an inbound call script in action in the short video below:

Ulrich also added these communications tips:

“Clarify the situation: In the context of loan and credit payment deferrals, you should inquire to what extent a customer is affected by COVID-19 (for example, reduced hours, self-employed, interruption of business). This query should be standardized and with selection options, not free text entries — otherwise, agents may face a mountain of individual answers that have to be laboriously evaluated.

“Check tools: Review your 'customer engagement toolbox', specifically your interactive and web portal / app channels to ensure they display all the current deferral options in connection with COVID-19.

“Coordinate communication: Review all texts in automated communication and in the guidelines for call center employees to make sure they are appropriate in the current situation. If the necessary sensitivity is lacking, this can lead to reputation damage.”

#5. Collections Analytics: Are We Missing The Credit Risk Revolution?

The fifth most popular collections and recovery post last year predates the pandemic. “Having worked in credit risk for most of my career during the revolution in analytics, it continues to concern me that the collections and recoveries (C&R) divisions of banks seem to be left behind,” wrote Jashan Augustine. “Innovations in credit risk analytics that have been widely adopted in other risk areas rarely get used at the C&R level.”

Jashan discussed the way that credit risk teams use risk models for multiple purposes — why not do the same with collections models? “In the collections case, using custom-created models can improve strategies by determining the prescribed channel – whether to call customers, SMS, email or leave them alone – that will result in the most effective use of the operational teams. The collections scores can also be used to determine the sequence of all actions – you could call at one instance, SMS a second, email a third and follow up with a call again. Some actions may be sequential, others concurrent – all in one day!

“Both the scorecard development and treatment strategy development follow similar tactics as in other parts of the credit risk lifecycle but with more granular adaptation for C&R. The treatment actions for the customers in collection can be highly dynamic, there is always something that can be done better and the value of doing so is often surprisingly high.”

Many of our bloggers closed with an open invitation to debt collection professionals: if you have questions about how you can maintain performance in the current environment, reach out to us at info@fico.com. We have people steeped in industry best practices who are seeing what’s happening around the world. We can help.

Popular Posts

Has the Reporting of Rental Data to the Credit Reporting Agencies (CRAs) Increased?

FICO Score 10T includes rental data, but consumers can only experience the benefit of this to the extent that their rental data is reported to the CRAs

Read more

FICO Statement on FHFA and FHA Updates to Credit Score Modernization

FICO supports FHFA’s announcement that the long-anticipated historical data for FICO® Score 10T will be released to the mortgage market.

Read more

Average U.S. FICO® Score at 716, Indicating Improvement in Consumer Credit Behaviors Despite Pandemic

The FICO Score is a broad-based, independent standard measure of credit risk

Read moreTake the next step

Connect with FICO for answers to all your product and solution questions. Interested in becoming a business partner? Contact us to learn more. We look forward to hearing from you.